California Wildfires, Property Damage, and Mortgage Repayment

California Wildfires, Property Damage, and Mortgage Repayment

California Wildfires, Property Damage, and Mortgage Repayment

Author: Siddhartha Biswas

Author: Mallick Hossain

Author: David Zink

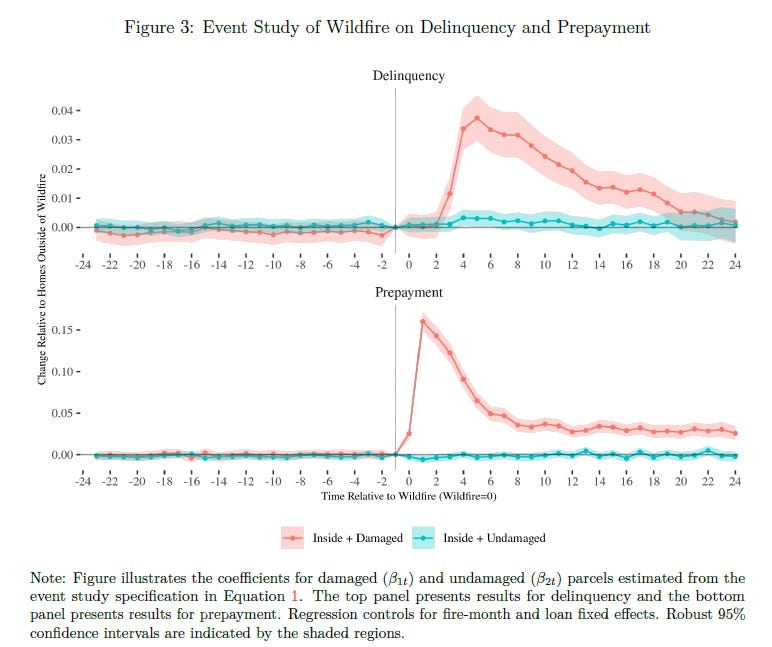

Abstract: This paper examines wildfires’ impact on mortgage repayment using novel data that combines property-level damages and mortgage performance data. We find that 90-day delinquencies were 4 percentage points higher and prepayments were 16 percentage points higher for properties that were damaged by wildfires compared to properties 1 to 2 miles outside of the wildfire, which suggests higher risks to mortgage markets than found in previous studies. We find no significant changes in delinquency or prepayment for undamaged properties inside a wildfire boundary. Prepayments are not driven by increased sales or refinances, suggesting insurance claims drive prepayment. We provide evidence that underinsurance may force borrowers to prepay instead of rebuild.

Date: 03/2023

URL: https://www.philadelphiafed.org/-/media/frbp/assets/working-papers/2023/wp23-05.pdf

Date Added: 3/27/2023, 6:57:38 AM

Reading Notes:

Objective: To understand the impact of wildfires on mortgage payments

Importance: Uses property-level data on wildfire damage, rather than fire perimeter, reducing measurement error relative to previous studies

Background: From 2017 to 2021 wildfires in California led to $16.8 billion per year in losses, an over tenfold increase compared to earlier years

Households may use insurance money to pay mortgages early

Data & Key Variables:

Monitoring Trends in Burn Severity (MTBS) - Wildfire burn perimeters (2013-2020). 82 wildfires that burn 1000+ acres and damage 1+ structures

CAL Fire Damage Inspection (DINS) database - Extent of damage by parcel

Corelogic public records - parcel locations, undamaged parcels

Federal Reserve FR Y-14M - mortgage performance history

Methodology: Difference-in-differences comparing homes within the fire perimeter (both damaged and undamaged) to houses 1-2 miles outside the perimeter

24 month window before and after fire

Results: Wildfires lead to large increases in delinquencies (~4 percentage points) for properties that are damaged, but no effect for undamaged properties within the fire perimeter.

Wildfires also increase mortgage prepayment for damaged properties (~16 percentage points), which may mean households are choosing to use the insurance money to walk away from the damaged home instead of rebuilding. This may be because the insurance doesn't provide sufficient funds to rebuild (underinsured)

Key Table/Figure: